Do you know how much over-age used car stock is costing you?

- Average weekly reduction from original advertised to final price is £40 to £50

- Transparency on aging stock is important for return on original investment

- Tricky balance between ‘easy’ cars and higher risk, potential higher margin cars

‘You lose an average £5.95 profit for each day a car doesn’t sell, up to 45 days.’ That’s a less familiar phrase, but it should be more widely known because that’s how much over-age stock is costing you. And that figure increases the more over-age a car becomes.

We all know buying the correct stock to meet consumer demand in your marketplace is the ideal scenario, although it often seems difficult to match supply with demand. For example, bringing cars into stock from part-exchange – even if they’re not ideal – will often be more desirable than having empty spaces on the forecourt or a lack of choice online.

When exactly is a car over-age?

The other tricky aspect of stocking is deciding how flexible to be on the question of when a car has become ‘over-age’.

I certainly would not patronise dealers who are doing well managing their stock with no black-and-white over-age policy. However, my previous experience as a dealer, along with the research I do these days, suggests many of us can sometimes be a little too attached to cars we have chosen for stock – even when they don’t seem to be drawing eyeballs. That’s why it’s important to understand the financial impact of hanging on for too long, rather than taking some quicker pain.

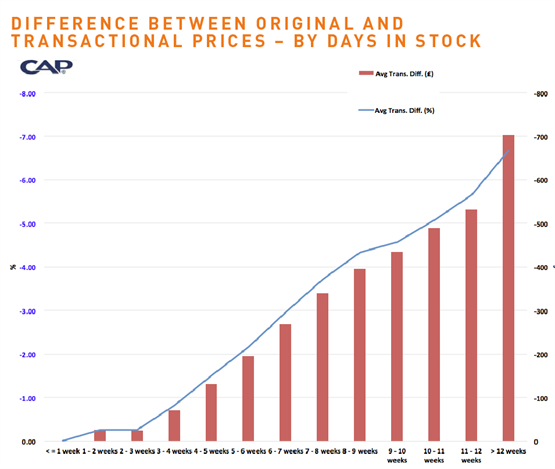

To better understand the relationship between return on investment and days in stock, I have been researching the difference between original advertised asking price and the eventual selling or transactional figures. Few will be surprised by the chart, right, which reveals that potential profit falls the longer a car outstays its welcome.

The difference between original and transactional prices – by days in stock:

At 45 days, the average daily reduction between the original asking price and what the vehicle sells for works out to be £5.95 - or £267.75 in total. The mean reduction increases to £6.58 a day at 60 days, giving a total of £394.80. By 90 days, the figure has increased to £7.82 a day – a total of £703.80.

When I took these figures into the market for feedback, the general sentiment was that an average of £40-£50 a week represents a ‘typical’ aging discount differential and that the bulk is weighted towards 9+ weeks, with the smallest figures at weeks one and two.

Dealers know the mix and management of stock is as important as the ability to sell cars. That’s why we constantly discuss issues such as the relative profitability of ‘easy’ purchases – vehicles that are invariably available in volume – contrasted with more costly, higher-risk investments that may require extra management. I suggest the calculation above may be useful in comparing the performance of these different types of stock. This is part of the discipline of a defined stocking policy, rather than the ad hoc approach.

Dealers are faced every day with the question of cost to their business of over-age stock. We all recognise the situation of a 90-day car, when your average days to sell are 51, and the need to understand what this is actually costing. To illustrate this, if the dealer’s average gross profit is £1,350 and it reaches 90 days in stock against an average stock turn of 51 days (it failed to sell 1.76 times), this would potentially equate to a cost of overage of £2,376. Based on the research carried out, your additional retail discount has amounted to £704 (£7.82 per day based on 90 days). Transparency around these kinds of costs is the best possible argument for the need to turn stock quickly to achieve maximum return on operational investment.

Of course, there are always factors outside our control, such as the quality and volume of stock available. For example, if quality stock is thin on the ground, it becomes harder to accept that a car you’ll find difficult to replace is truly over-age. But disciplined discount policies and managing the stock without emotional attachment is generally going to deliver increased returns on your investments.

The right data is what makes the difference between optimal profit and doing ‘ok’. That means data about your own performance, your customers and the prices advertised by your competitors. The days of emotional attachment to cars we thought were perfect for stock, but haven’t sold yet, are over.

So are the days of pricing our stock at what we think it’s worth – not what your customers expect to be paying. But more about that another time.