Is this the calm before the storm for used values?

At the time of writing the market is performing well; prices at auction are holding up as buyers are still actively seeking stock. As a result average conversion rates remain around 70%.

As always the Black Book Editorial team have been keeping their ears close to the ground and as we arrive at the middle of the month, latest reports are that one of the UKs largest auction halls, BCA Blackbushe, is busy – lots of cars and lots of buyers; a positive sign for the used car market. When the editor has trouble finding a parking space, it’s always a sign!

The big question is whether supply will outstrip demand? More part-exchanges will be appearing in the market, as they now start to arrive as a result of new car activity due to the “64” plate. Will so many buyers remain keen to purchase stock? It has been particularly noticeable that even the franchised dealers that traditionally concentrate on selling new cars in September, and have plenty of part-exchanges to fill their used pitches, are active at auctions.

In the first 2 weeks of September there have only been low levels of depreciation noted overall within our data. This is as expected, as it is usual for there to be a time-lag from the start of September before used volumes increase. Convertibles are the cars under the most amount of pressure, down 1.5% month-to-date at the 3-year, 60,000 mile point. As we start to enter autumn, SUV prices generally increase, as long as there is not over-supply, and this year has been no different – values are up 0.3% month-to-date at the time of writing and expected to continue rising. Other sectors sit somewhere in between with regards to movements.

Watch this space – will the inevitable increases in volumes of used cars available in the market put pressure on price and if so, by how much? Black Book Live will be reporting any changes as they happen.

*month-to- date @ 3 years and 60k miles

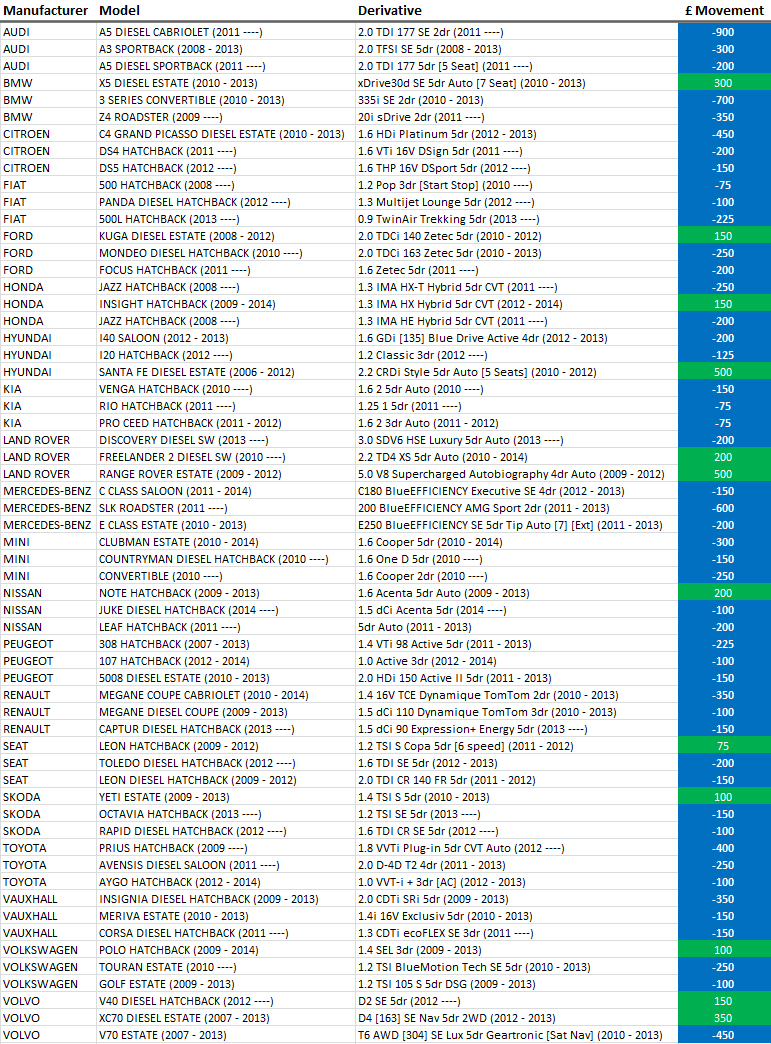

** For exact derivatives see the table below