Sourcing stock - are you now going direct to the consumer?

The results of the latest Dealer Survey for June 2015 are in...

As we come to the end of the second quarter of 2015, and reach the half way stage in the year, in the main it can be described as a ‘normal’ June.

There are without doubt some challenges and pressures however. Volumes through used cars are rising, and along with an increase in retail competitiveness and rising costs, this is causing pressure on retained margins in certain operations. The continual focus on consumer incentives from the manufacturers continues to intensify by the end of the quarter and half way stage.

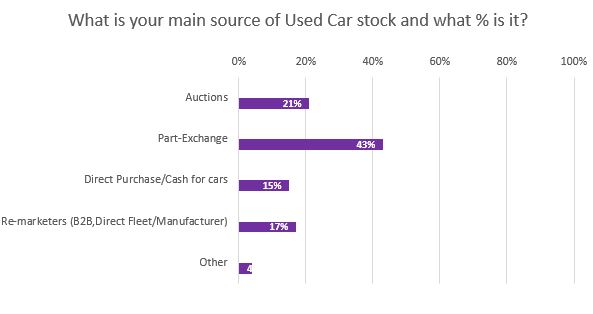

A clear observation this month is how diverse the network is at sourcing their stock. There is a large variance between those who are reliant on auctions, to those spreading their wings and sourcing direct from the consumers.

Other noteworthy changes:

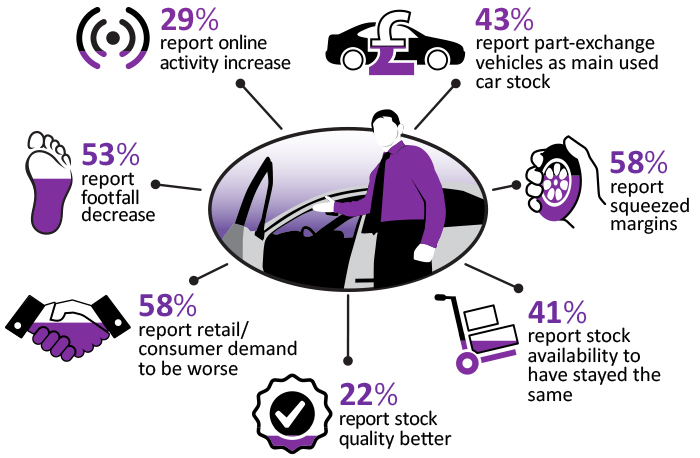

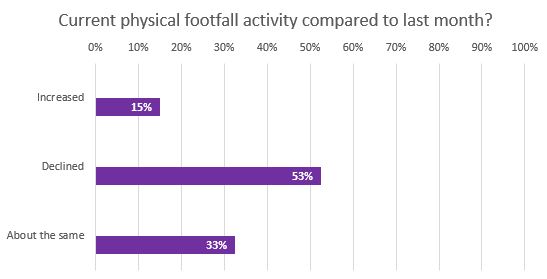

- A rise in June in those reporting an increase in footfall of 15% from 9% in May. However half are experiencing a decline – with the remaining third seeing no change.

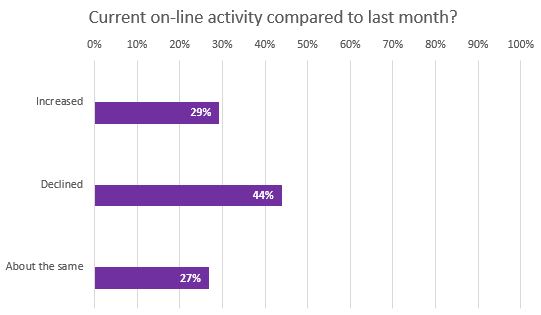

- A notable change from May is that 30% are enjoying an increase in online activity, up from 18% in May. The remainder are either not seeing any change or have felt a slight slowdown.

- The pressure on retained margins looks to be continuing throughout June as 58% of those responding indicated they were being squeezed – an increase from 41% in May. Sentiment suggests that the increased competitiveness caused from greater volumes of available stock and costs are putting pressure on profitability.

- Interestingly those reporting an increase in stock availability has eased slightly from 52% to 38% in June; whereas a number felt that it had actually deteriorated over the month - from 9% to 20%. However just under half felt that there was little or no change from last month.

- As in May, the quality of stock remains reasonably stable, with the majority of 63% reporting no change from last month. However those experiencing a decline in quality increased by 4%.

- This month there is little to separate those who feel that the current trade values are reflective of the market, with 48% reporting they are and 50% feeling they are too high. What’s certain is that only 3% felt they were too low. This question is very subjective, as it is very much dependent on where they are sourcing stock and what sector into the market they are operating within.

- As we approach the half year stage over half the dealers feel that retail and consumer demand has eased slightly from last month. However those reporting an increase remains in double figures.

- Reviewing where dealers source their used car stock is without doubt very diverse, dependent on the business strategy and sector within the industry they operate in. From those surveyed, 42% of their stock was sourced via natural part-exchanges. However the remainder was split across various sources. Auctions accounted for only 21%; whereas 15% of stock purchased is now sourced via Direct Purchase or Cash for Cars processes and the other stock is from areas such as Trade-to-Trade, Manufacturer Direct sales or Direct ex-fleet. This is a question which would be useful to review again as the year progresses to observe whether this ratio changes over time.

The Market Survey – for Dealers, by Dealers

Why has this survey been done?

This market survey has been created in response to dealers hankering for a more holistic current sentiment of the questions they ask themselves daily, so they can understand the temperament of the wider market.

Who is it for?

Respondents cover a very diverse sector of the automotive industry, from the larger franchise groups, supermarkets, independents, single site owner-driven operations, through to auctions and remarketing.

When is it undertaken?

The survey is done monthly, within a very small open window. This ensures that the responses are market relevant and current. The data in this survey is for June 2015.

Get involved!

If you want to be involved in next month's Dealer Survey – for Dealers, by Dealers - then please contact CAP's Black Book Editor and Retail & Consumer Specialist, Philip Nothard.

philip.nothard@cap.co.uk

07702 382025