LCV Editorial October 2014

LCV Marketplace

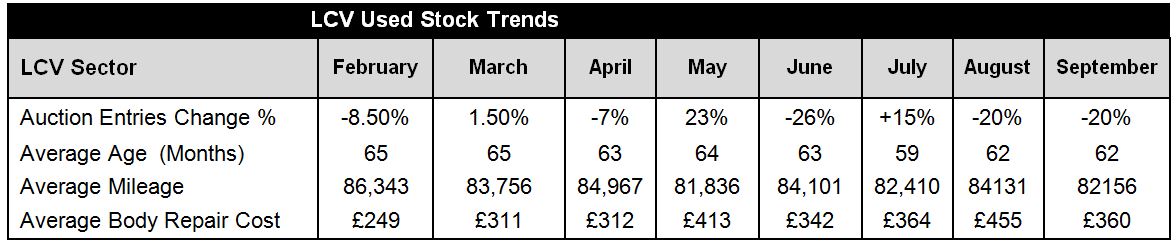

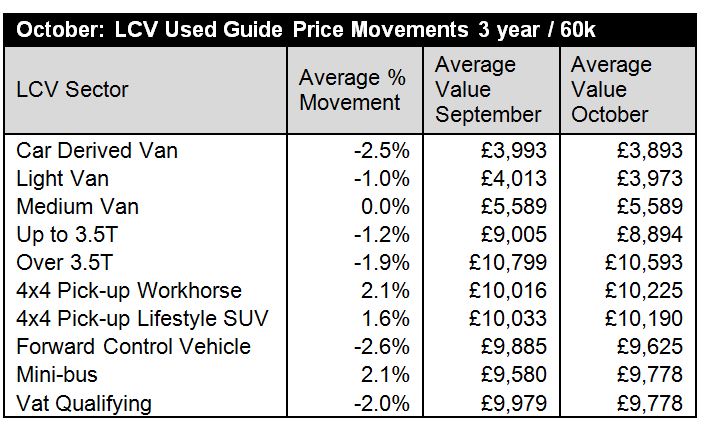

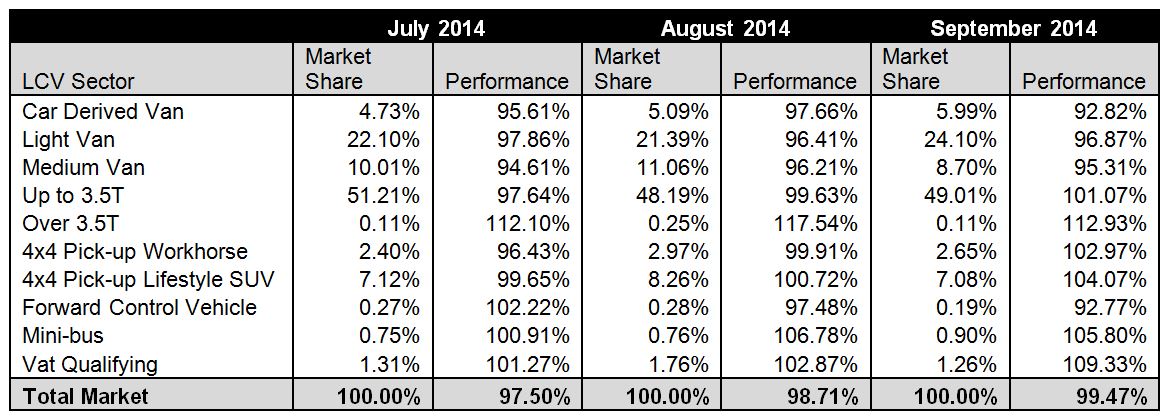

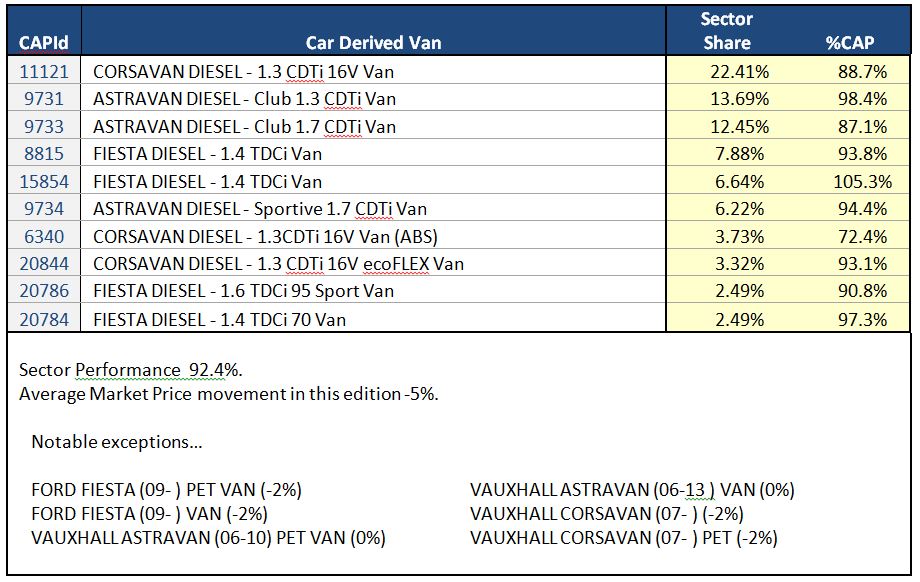

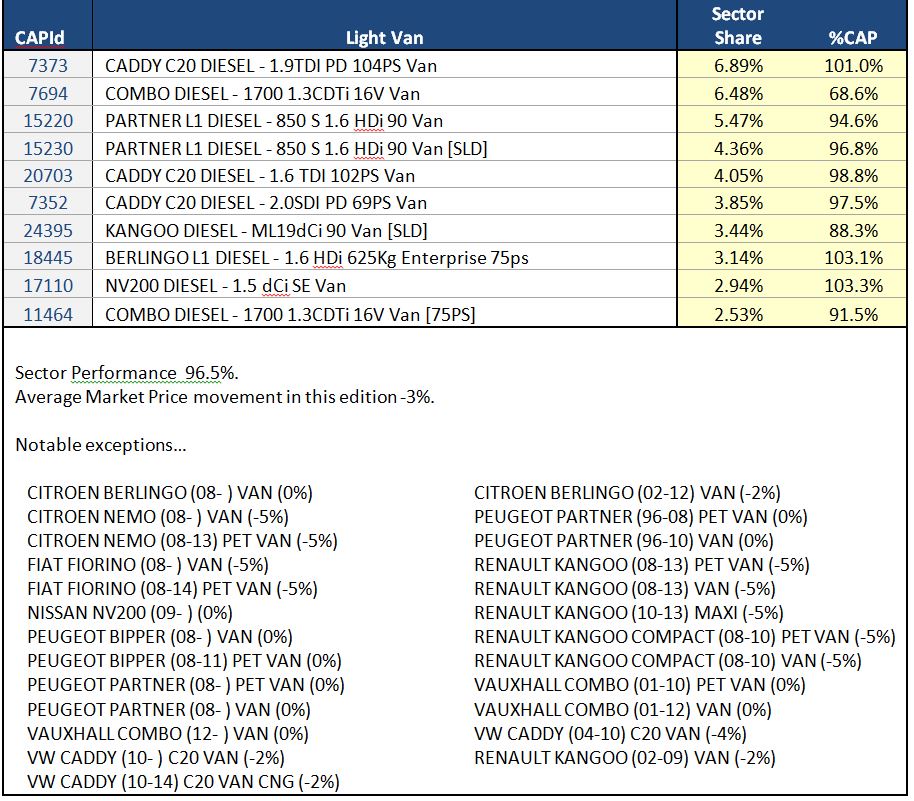

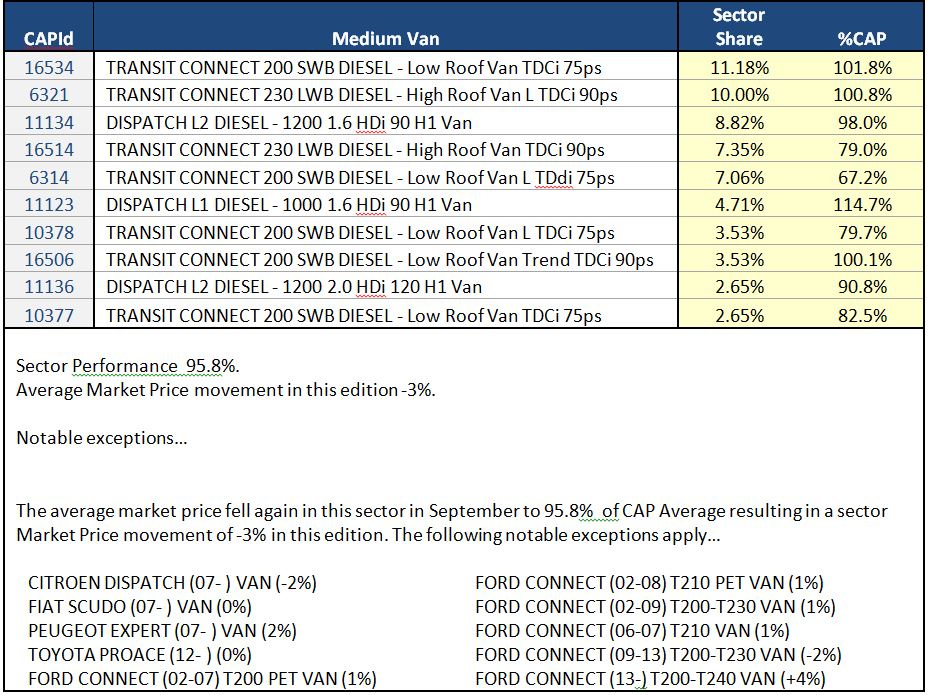

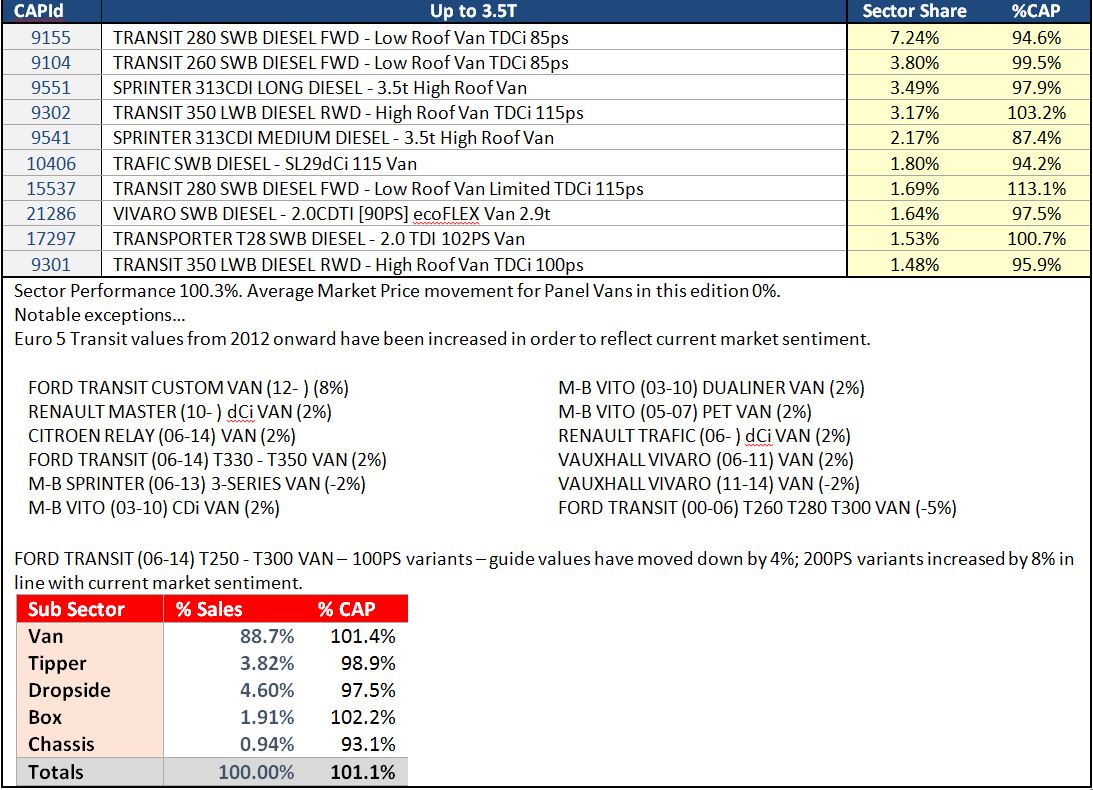

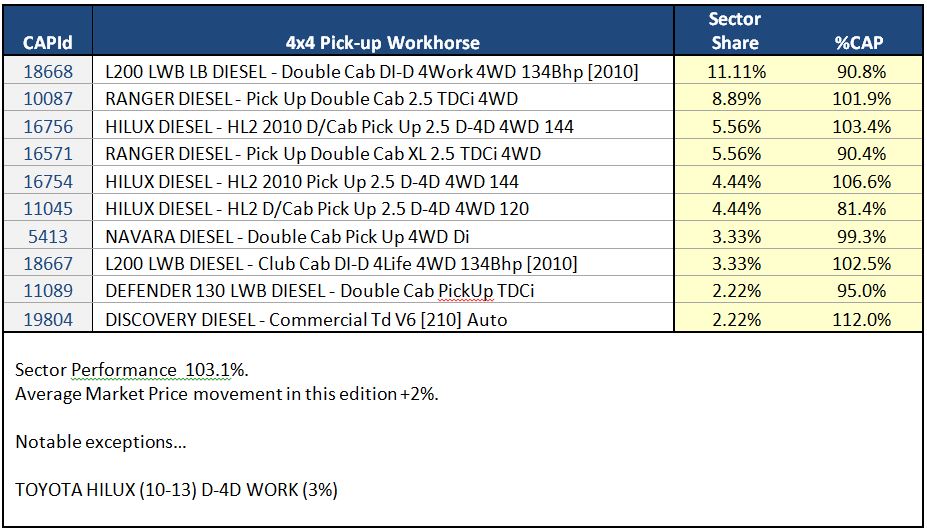

As the summer holiday season drew to a close September got off to the usual slow start that we have historically come to expect in the used LCV wholesale market. According to the data we receive from all the main auction centres across the UK, during the first week sales were down by 5% when compared with the average weekly sales for August, whilst auction entries were up by 11.3%. Only around 70% of the vehicles presented for sale actually sold and on average they were making around 2% less than the CAP Average guide price. Whilst the auctions we attended were reasonably busy, many familiar faces seemed to be missing and the Internet was uncharacteristically quiet. Things picked up considerably by the second week and at most of the sales we attended there was a definite buzz in the air. Attendance levels were much higher and there was a healthier mix of end users and professional buyers competing against a torrent of stealthy internet buyers for the best lots. With auction sale catalogues looking decidedly thinner and comparatively low entries from some of the larger vendors it soon became apparent that limited stock was the main driving force behind this resurgence. According to our research auction entries were down by around 20% in September when compared to August and, whilst the average age remained the same at 62 months, the average recorded mileage decreased from 84,131 to 82,156. From our own independent vehicle inspections the average repair cost for body panel damage on vehicles presented for sale decreased from £455 to £360 over the month. However, it was noticeable that a larger proportion of vehicles were exhibiting body and paint damage. Looking at the LCV sectors, Car Derived, Light and Medium vans under-performed significantly but stock was severely limited and many examples were in poor condition. On the other hand large vans in the 2.5t to 3.5t GVW range fared much better and many seemed to be selling around the guide price irrespective of condition. This is a strong indication that there are insufficient numbers in the used market to meet the current level of retail demand. Similarly, Minibuses appeared to be back in favour with strong bidding for both 15 and 17 seat models. Last month we said that so far this year, we haven’t really been able to detect the traditional seasonal buying patterns that affect market prices. No better example of this can be found than in the 4x4 Pick-up Sector. There were plenty of examples of both Workhorse and SUV Lifestyle models selling well above guide prices sectors raising the average sales performance by around 3% at time when demand is normally flat. With guide values falling month on month since March, apart from last month when there were a few marginal increases on some models, it seems that market prices have now reached a level that’s indicative of their true worth and offer savvy dealers with a profit opportunity not to be missed.